Join Ust. Usman Malik and Dr. Bilal Philips for an exclusive webinar on Islamic Investments

Navigating Wealth: A Strategic Analysis of Islamic Investment Opportunities in the West

Abstract

This synopsis details the comprehensive framework for achieving financial stability and prosperity in Western economies while strictly adhering to the principles of Islamic jurisprudence (Sharia). In a presentation delivered by Dr. Bilal Philips, the core challenge of reconciling contemporary financial practices with the prohibition of Riba (usury) and Gharar (excessive risk/speculation) is addressed. The analysis moves beyond mere avoidance, outlining proactive, strategic avenues—including profit-and-loss sharing models, asset-backed finance, and community-focused endowments—that ensure investments are both Halal (permissible) and contribute to the broader welfare (Maslahah) of the Muslim Ummah. This paper serves as an essential resource for those seeking guidance on Sharia-compliant investment, Islamic finance, and ethical wealth management in non-Muslim majority contexts.

I. Foundational Framework: The Synthesis of Wealth and Deen

The Islamic approach to wealth is one of regulation, not prohibition. Dr. Bilal Philips emphasizes that while acquiring wealth is permissible, it must be guided by divine principles. The fundamental pillars of the Islamic economic system are built upon the prohibition of Riba (interest, both simple and compound) and Gharar (uncertainty or excessive speculation). Unlike conventional banking, which guarantees a return regardless of the underlying enterprise's success, Islamic finance necessitates a partnership rooted in Profit and Loss Sharing (PLS), primarily through instruments like Mudarabah (trustee finance) and Musharakah (joint venture partnership).

A critical ethical filter is imposed on all financial activities: investments must be directed toward permissible (Halal) sectors and must avoid involvement in industries such as alcohol, pork production, gambling, or armaments. This ethical framework ensures that financial stability is achieved within a moral and socially conscious structure.

II. Strategic Avenues for Sharia-Compliant Investment

The challenge for Muslims residing in the West is the scarcity of accessible, genuinely compliant investment products. Dr. Philips underscores the need for genuine innovation to move past superficial Sharia adjustments on conventional instruments. The presentation identifies two established and resilient investment avenues:

1. Tangible Assets: Islamic Real Estate Investment

Historically and presently, Islamic real estate remains one of the most reliable and tangible assets for Sharia-compliant investment. The nature of real estate allows for financing structures that circumvent Riba. This is typically achieved through:

• Murabahah (Cost-Plus Financing): The financier purchases the asset and sells it to the client at a predetermined marked-up price, payable in installments, eliminating the debt-interest relationship.

• Ijarah (Leasing): A lease-to-own structure where the financier retains ownership and the client pays rent, leading to eventual transfer of ownership.

Despite its inherent compliance, caution is advised regarding transparency in contracts and ensuring that rental income is not derived from impermissible activities.

2. Capital Markets: Islamic Stock Screening

For individuals with liquid capital, the stock market presents a viable option through rigorous Islamic stock screening. This dual-criteria screening process ensures compliance:

• Business Sector Compliance: The core operations of the company must be Halal.

• Financial Ratio Compliance: The company's financial structure must meet specific thresholds regarding debt, cash, and receivables relative to its market capitalization or assets.

Dr. Bilal Philips notes that recognised indices, such as the Dow Jones Islamic Market Index (DJIMI), offer a baseline for investors. Crucially, the process demands continuous diligence; Islamic investment is a dynamic strategy, not a passive "set it and forget it" approach, as companies' financial ratios can fluctuate in and out of compliance.

III. Community Development and Future Directions

The webinar highlights investment opportunities that offer a dual return—financial growth and social benefit (Maslahah):

• Ethical and Sustainable Ventures: Investments aligned with sustainable principles, such as renewable energy, responsible agriculture, and community-serving technology, naturally harmonize with Islamic values. These avenues provide both financial profit and a contribution to the long-term welfare of the community.

• Modern Waqf (Endowments): Waqf, traditionally an act of perpetual charity (Sadaqah Jariyah), can be structured in modern forms to create self-sustaining community assets (e.g., educational facilities, social housing). While not strictly commercial investment, these instruments secure long-term communal welfare and offer spiritual reward.

Finally, the purification of wealth through Zakat is stressed as a critical mechanism for annual economic redistribution. Dr. Philips underscores that proper investment facilitates the growth of Zakat-eligible wealth. Given the complexity of contemporary contracts, the importance of consulting qualified Sharia advisors is paramount to avoiding Shubuhah (doubtful matters) and preserving the sanctity of one’s earnings.

Conclusion

The pursuit of financial prosperity in Western economic environments is entirely compatible with Islamic principles, provided that the investor is equipped with knowledge and diligence. Dr. Bilal Philips concludes that the successful path is paved by strictly avoiding Riba and Gharar, prioritizing tangible and ethical investments like real estate and screened equities, and contributing to the communal good through structures like modern Waqf. The ultimate aspiration of Islamic financial stability is not maximizing material profit, but attaining Barakah (blessing) by ensuring all financial actions serve one's Deen.

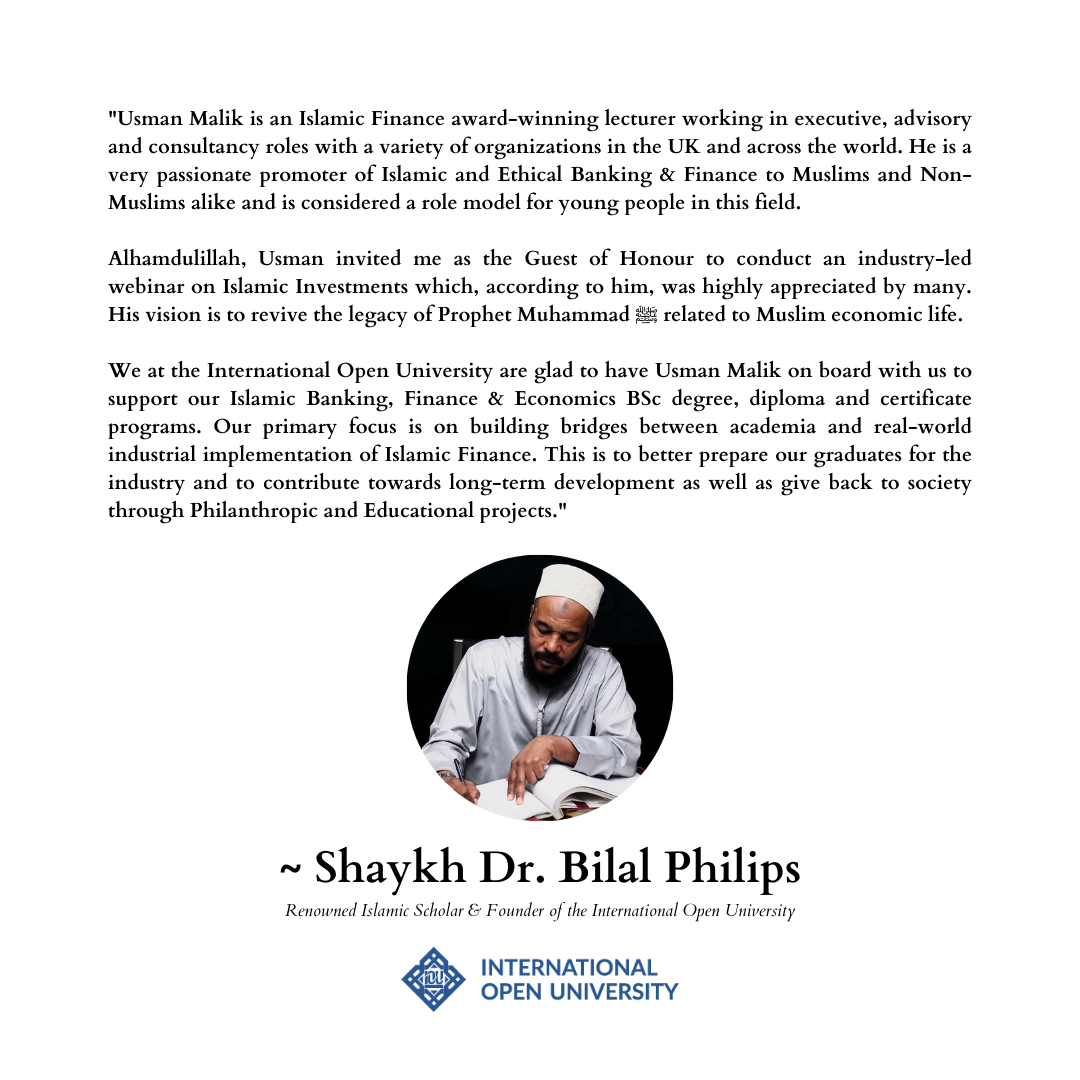

Endorsement by Shaykh Dr Bilal Philips

Support our Da'wah

Share Islam with the World

Share Islam with the World